At the annual Africa International Housing Show (AIHS) in Abuja, the narrative surrounding Nigeria’s housing deficit took a sharp, definitive turn. Speaking at the “FMBN Day” plenary, Shehu Osidi, the Managing Director of the Federal Mortgage Bank of Nigeria (FMBN), delivered a data-backed progress report that caught the attention of players across the continental housing ecosystem.

Between 2024 and 2025, the apex mortgage bank successfully financed and delivered exactly 9,076 housing units across the federation.

For a nation historically trapped in systemic housing deficits and stiff equity requirements, the numbers reveal a clear operational shift.

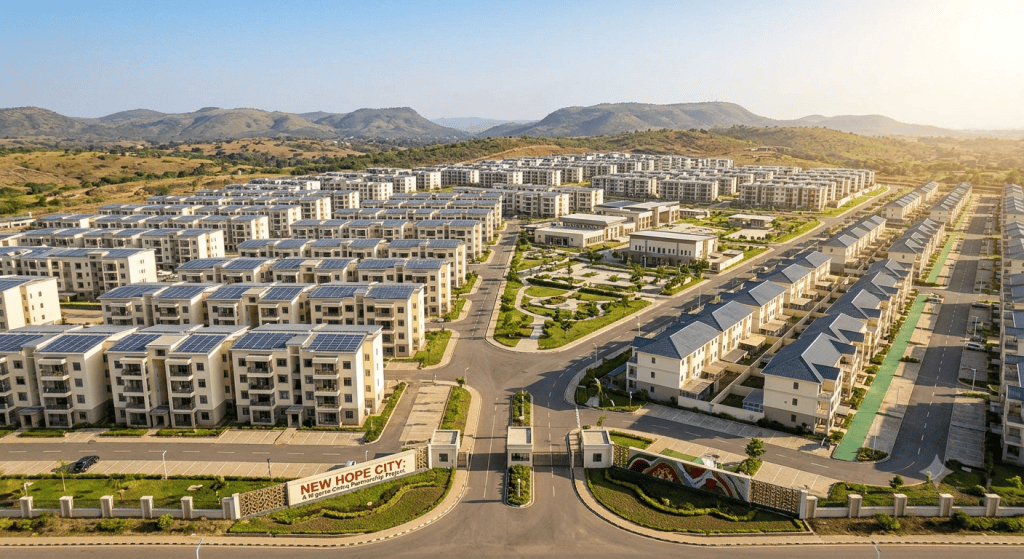

Gemini generated image to illustrate affordable housing units

The Velocity Breakdown: A 300% Multiplier

The headline figure is less about steady growth and more about a sudden acceleration. The bank’s performance shows an aggressive spike in housing delivery within a 24-month window:

2024 Delivery: 2,165 Units

===================================

2025 Delivery: 6,911 Units (96% of Annual Target)

This sudden momentum, representing an approximate 300% year-on-year increase in funded properties, was structurally enabled by a massive ramp-up in construction finance. Project loan disbursements swelled from ₦31.5 billion in 2024 to a historic ₦79 billion in 2025. This capital injection directly unlocked key residential schemes, including massive co-funded off-taker guarantees for President Bola Tinubu’s Renewed Hope Cities and Estates programme.

| Key Interventions Under the Renewed Hope Agenda | Approved Funding |

| Ibeju-Lekki City Project, Lagos | ₦27 Billion |

| Karsana City Project, Abuja | ₦19.9 Billion |

| Port Harcourt Urban Scheme | ₦10 Billion |

| Enugu Residential Development | ₦7.8 Billion |

Macroeconomic Ripples: Beyond the Brick and Mortar

During his AIHS presentation, Osidi reminded stakeholders that the bank’s interventions carry economic impacts far beyond the physical structures.

“Beyond the numbers, these investments represent thousands of jobs created for artisans, engineers, architects, quantity surveyors, suppliers, transporters, and numerous small businesses operating within Nigeria’s housing value chain,” Osidi stated.

The economic footprint of injecting over ₦79 billion into local construction projects manifests in three major ways:

- Direct and Indirect Labor Absorption: Laying foundations for nearly 7,000 units in a single year requires localized workforces. Thousands of bricklayers, electricians, plumbers, and manual laborers found consistent employment, stimulating micro-economies across various geopolitical zones.

- Domestic Supply Chain Reinforcement: The procurement of building materials, such as locally manufactured cement, rods, roofing sheets, and timber, provided essential revenue for local manufacturers and building merchants wrestling with macroeconomic inflation.

- Financial Inclusion & Recirculation: National Housing Fund (NHF) collections reached an all-time high of ₦152.4 billion in 2025 (a 48% increase from 2024). Concurrently, home renovation loan programs alone disbursed ₦13.8 billion to over 15,000 beneficiaries. This represents a democratic redistribution of capital directly into property upkeep and localized retail commerce.

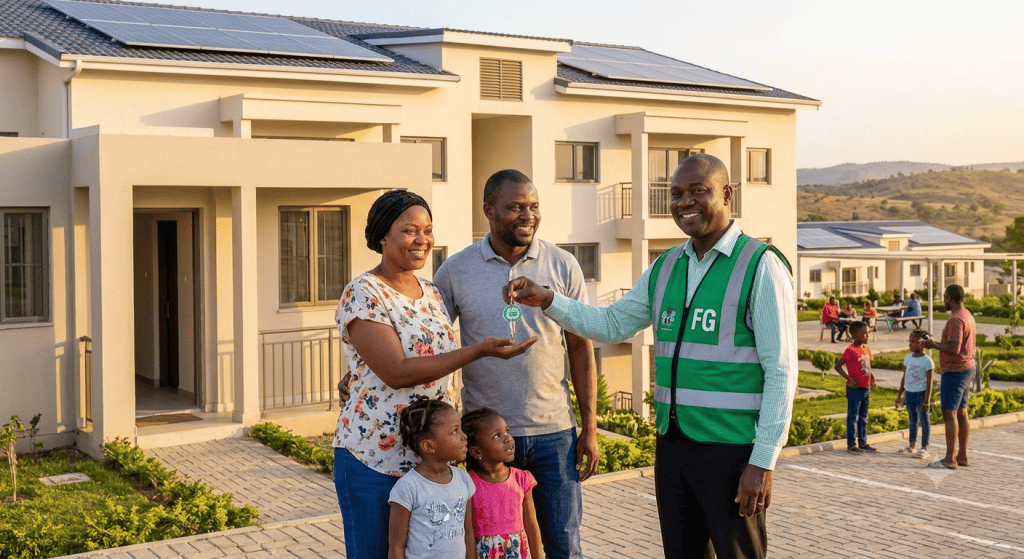

Gemini generated image to illustrate the delivery of affordable housing units.

Redefining the Future of Affordable Housing

For decades, formal housing finance in Nigeria operated on conventional banking assumptions: steady salaries, formal documentation, and hefty upfront equity. However, informal sector workers make up more than two-thirds of Nigeria’s workforce. As Osidi noted, these are the very citizens who contribute heavily to national productivity yet remain fundamentally excluded from standard mortgages.

To correct this, the future of affordable housing in Nigeria relies on two distinct strategic shifts outlined by the FMBN leadership:

1. Tailored Underwriting for Informal Realities

The bank has rolled out non-interest mortgage options, diaspora NHF products, and rent-assistance loans specifically structured around irregular or non-traditional income patterns. By removing the steep hurdle of immediate down payments, schemes like the FMBN Rent-to-Own product allowed 367 households to transition seamlessly into properties valued at over ₦7.1 billion through predictable monthly payments.

2. Multi-Stakeholder Consortia

The scale of Nigeria’s housing deficit cannot be closed by public budgets alone. The current momentum rests on structured partnerships. By combining FMBN capital with aggressive state government buy-ins (such as Kano State re-entering the NHF scheme after a 20-year hiatus), organized labor, and private developers, the institution is establishing a scalable blueprint for mass housing.

As the six-day AIHS summit concluded, the main takeaway was clear: building 9,076 homes proves that with operational adjustments and better funding mechanisms, affordable housing in Nigeria can transition from an elusive policy goal into a repeatable reality.

{kind=link}